“Big Short” investor David Burt’s new bet: Global warming will bust the housing market – “You end up with a very scary looking situation”

By Geoff Dembicki

1 November 2019

(Vice) – In 2007, almost no one would admit what became obvious in hindsight: The housing market was on the brink of collapse and would take a good chunk of the U.S. economy along with it. Lenders were getting rich, giving home loans to people who couldn’t afford them, investment banks were making a killing by combining those shaky loans into securities, ratings agencies cashed in by certifying those securities as safe and millions of ordinary people got screwed when the whole thing came crashing down.

But David Burt saw it coming. The investor was a consultant at Cornwall Capital, the firm that shorted the subprime mortgage market and made $80 million as some of Wall Street’s biggest firms imploded around it. It was such a spectacular, farsighted bet against the conventional wisdom surrounding the housing market boom that Cornwall was profiled in Michael Lewis’s book The Big Short, and one of Burt’s colleagues was played by Brad Pitt in the movie adaptation. The thing, though, is that many of the risk factors leading up to the crash were fairly easy to spot if you weren’t earning massive profits dependent on ignoring them.

“There’s some really big incentives problems in markets,” Burt explained recently at a hotel café on New York’s Upper East Side. “Whether it’s conscious or subconscious, and it’s not necessarily nefarious, a lot of the time it’s just easier for people to do the thing that’s best for them in some easy-to-conceive-of timeframe.”

The bet I’m making is that many regional markets will experience large price declines in response to increasing costs related to the geography-specific risks.

David Burt, CEO and Founder of the investment firm, DeltaTerra Capital

Now Burt thinks there could be another financial disaster growing inside the real estate market. But this time, the bubble is being inflated by climate change denial.

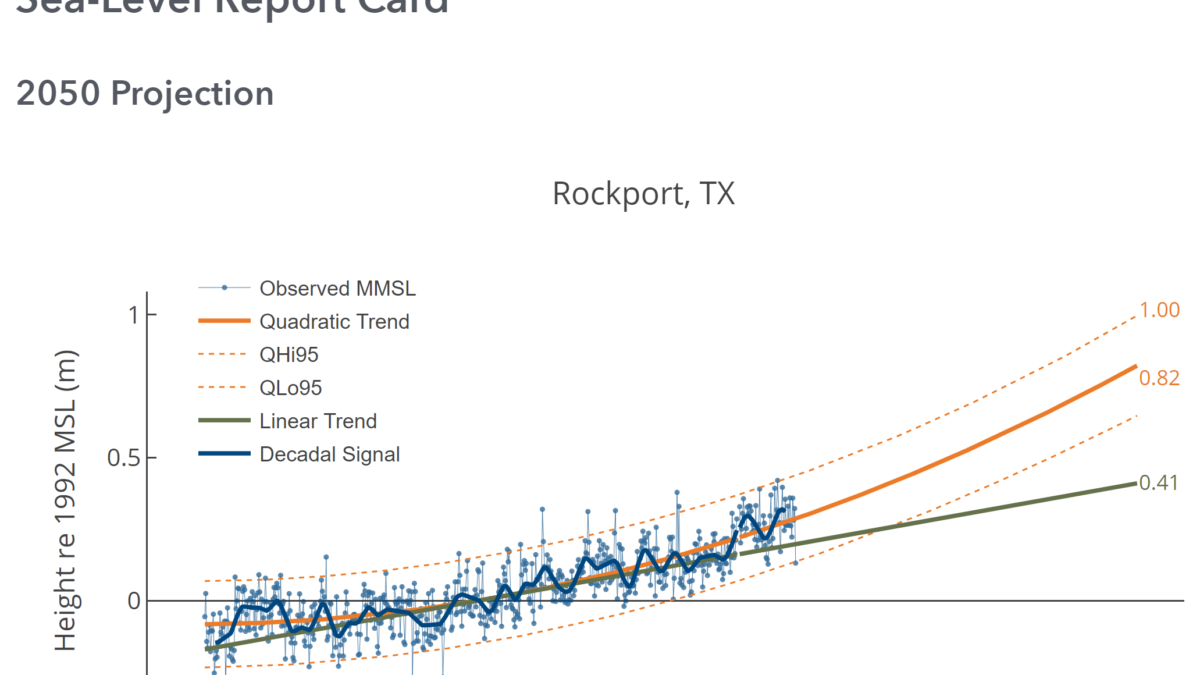

We tend to conceive of global temperature rise as a slow, steady and predictable threat: humans release emissions, the atmosphere gets warmer and sea levels get higher and higher. But the disaster Burt thinks the markets are ignoring could strike a lot sooner and more abruptly. It would likely be felt first in Texas, Florida, New Jersey, California or anywhere else with a ton of homes and other real estate exposed to flooding, and then spiral outwards into the financial system, potentially wreaking destruction rivaling what happened in 2008.

To understand the mechanics of this threat it helps to visualize the market for coastal real estate as a brand new condo tower on the beach. The foundations for this tower are built upon maps drawn by the federal government that seriously downplay the likelihood of sea-level rise and floods. The lower floors are filled with homeowners paying off mortgages on homes that could be chronically flooded within the next few decades. The penthouse is occupied by banks and other investors turning those mortgages into ever more complex investments. Though it’s hard to predict a specific event that knocks this tower to the ground—perhaps it could be a devastating $1 trillion Florida hurricane, or a stampede to the exits by investors once denial of climate dangers turns to fear—it’s clear to anyone paying attention that the entire structure is teetering in the ocean wind.

Burt sees similarities between now and the lead-up to 2008. “There’s a lot of parallels, it’s a big real estate mispricing issue. At its core that presents a lot of the same risks. A lot of real estate is massively overpriced and there’s a lot of risk associated with that and the big risk is another foreclosure crisis,” he said. “Now, it’s a very different dynamic that’s creating the mispricing but actually magnitude-wise it looks pretty similar, maybe even bigger.”

Like he did before the last crash, Burt has left his full-time investing job, this time at the $1 trillion Wellington Management. He now heads an investment firm which is focussed on financial opportunities in a real estate market threatened by climate change, some of which could materialize as early as next year. This places him in a similarly complex moral position—a plunge in housing values due to the market either collapsing or else accurately pricing the true risk of flooding might be terrible for millions of people, but also creates the chance for smart investors to earn a lot of money. Just as Cornwall cashed in while people lost their homes, Burt could profit in the aftermath of a devastating financial storm.

Though this is far from a mainstream perspective on Wall Street, he’s not the only prominent insider warning of the gigantic financial risks of climate change. “There will be ongoing, massive events, weather events, taking place, exposing potentially trillions of dollars of real estate to coastal flooding and damages,” Ed Delgado, a former executive at the mortgage entity Freddie Mac, told CNBC earlier this year.

Yet the market is acting as if climate change doesn’t exist. Anywhere between $60 billion to $100 billion worth of mortgages for coastal homes are issued each year. “We’re continuing to build in these flood hazard zones,” said Matthew Eby, founder and executive director of the First Street Foundation, a non-profit research group that studies flood risk. “You end up with a very scary looking situation.” [more]

A ‘Big Short’ Investor’s New Bet: Climate Change Will Bust the Housing Market

Citing climate risk, investors bet against mortgage market

By Kate Duguid

29 September 2019

NEW YORK (Reuters) – David Burt helped two of the protagonists of Michael Lewis’ book The Big Short bet against the U.S. mortgage market in the run-up to the 2008 financial crisis. Now he’s betting against the market again, but this time, the risk is not from underwater subprime mortgages, it’s from homes sinking under water.

As he did then, Burt has given up his full-time job to make that bet. He left his role as a portfolio manager at the $1 trillion Wellington Management last year to start an investment firm, DeltaTerra Capital, which aims to help clients manage climate risk, and, where possible, take advantage of ways the market has not yet priced in that risk. His first investment strategy is targeting residential mortgage-backed securities, or RMBS, with exposure to climate hot spots like Texas and Florida.

In doing so, Burt is joining the ranks of a small number of investors who have become worried that climate risk is underpriced in these securities, which are pools of home loans sold to investors.

“The market’s failure to integrate climate science with investment analysis has created a mispricing phenomenon that is possibly larger than the mortgage credit bubble of the mid-2000s,” Burt wrote in a presentation to prospective clients.

Most mainstream investors remain skeptical of the impact of climate change on their portfolios or argue that they are diversified enough not to have to worry about the risks.

Burt and at least three other investors said in interviews with Reuters that they think the risk is real. They argue that a growing body of academic research and data shows that hurricanes, flooding and other disasters pose a far larger threat than is currently being priced into mortgage securities.

“I don’t think you need any new climate effects to come to draw these conclusions. The ones I see happening right now, I just need to get a little unlucky with them and I’m in trouble,” said Thomas Graff, head of fixed income at Brown Advisory. Graff abandoned a riskier type of RMBS after Hurricane Harvey hit Houston in 2017.

Climate researchers and investors say a key culprit for the mispriced risk in the U.S. mortgage market is outdated flood maps drawn by the federal government.

These maps determine the premiums on government-sponsored home insurance policies. Due to budget cuts, more than three-quarters of the maps have not been updated in at least five years, according to First Street Foundation, an organization that is developing a publicly accessible database of up-to-date flood risk information.

Outdated maps mean far fewer people are required to have flood insurance than are at risk, the investors and researchers say. A University of Bristol estimate put the actual figure at around three times the 13 million Americans currently living in designated flood zones.

The gaps are evident: About 70% of all damages to homes that were flooded during Harvey were not covered by insurance, according to CoreLogic. […]

“The bet I’m making is that many regional markets will experience large price declines in response to increasing costs related to the geography-specific risks,” Burt said. [more]