The junk debt that tanked the economy? It’s back in a big way.

By Steven Pearlstein

27 July 2018

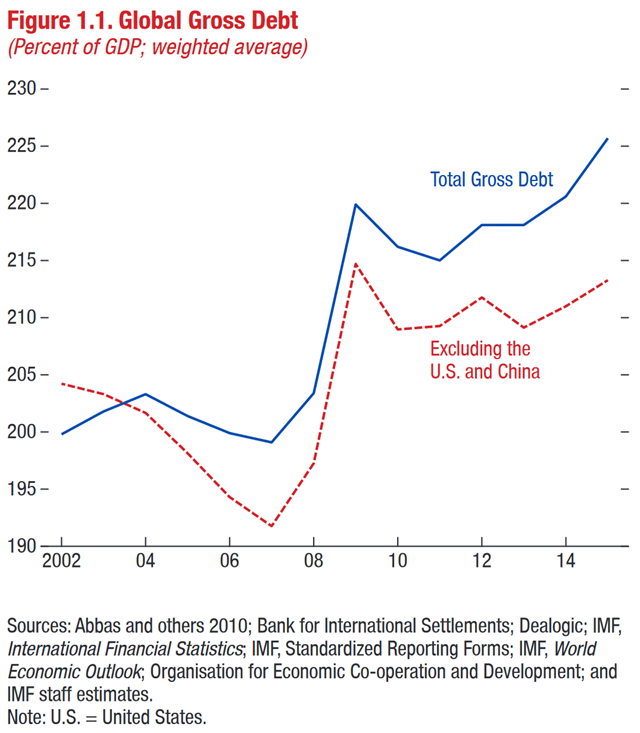

(The Washington Post) – Like most people, you probably assume that the level of lending done by banks at any moment is largely driven by how much demand there is from borrowers. But in the world of modern finance, that’s only part of the story. For just as important is the level of demand from investors — pension funds, hedge funds, mutual funds, sovereign wealth funds and insurance companies — to buy the loans that banks make. Indeed, there are times when there’s so much demand for loans from investors and the profit from selling them is so lucrative that bankers are only too happy to go out and make bigger and riskier loans than they would if they were keeping them on their own books. [cf. IMF says global debt tops all-time high at $152 trillion. –Des]

That was the situation back in 2006 when investors were so keen to own “mortgage-backed securities” that Wall Street was begging lenders for more and more “product.” You know how that turned out.

Now it is happening again, as investors and money managers scramble to buy floating-rate debt — debt offering interest payments that will increase as global interest rates rise, as they are expected to over the next few years.

A big new source of floating-rate credit is the market for “leveraged loans” — loans to highly indebted businesses — that are packaged into securities known as “collateralized loan obligations,” or CLOs. Because the market seems to have an insatiable appetite for CLOs, leveraged lending and CLO issuance through the first half of the year are already up 38 percent over last year’s near-record levels.

Credit-rating companies such as Standard & Poor’s and Moody’s have recently warned that this surge in corporate borrowing and lending has led to a noticeable decline in the quality of the loans. The borrowers have lower credit ratings. The loans contain fewer of the standard conditions that are meant to protect lenders. And the rating companies calculate that lenders should expect to recover less of their money if the borrowers default or go into bankruptcy.For the most part, however, these warnings have gone unheeded. […]

It is no coincidence that the decline in loan quality has occurred as there’s been a shift in who is doing the lending. Back in 2013, 70 percent of the loans were made by major banks whose lending is closely scrutinized by government bank regulators. That figure is now down to 54 percent, according to Bloomberg, as hedge funds, private-equity firms, insurance companies and non-regulated lenders have entered the market in a big way.

This shift in market share away from banks mirrors what happened to mortgage lending in the run-up to the 2008 crash, when competition from unregulated lenders led banks to lower lending standards in an effort to maintain their market share. [more]

The junk debt that tanked the economy? It’s back in a big way.